Personal Finance: My Journey from Pocket Money to Smart Money Management

⏱ 5 min read

When people hear personal finance, they often think of complex stock market charts, tax-saving hacks, or long financial planning spreadsheets. But for me, personal finance started way before any of that it started with pocket money and a lesson from my parents that shaped my money habits forever.

What is Personal Finance?

At its core, personal finance is simply how you manage your money—earning, saving, investing, and spending wisely. It includes:

- Budgeting (planning where your money goes)

- Saving & Investing (growing your wealth over time)

- Debt Management (keeping loans under control)

- Emergency Fund Planning (being prepared for the unexpected)

One of the most defining Gen Z characteristics is how effectively they spend their money. They’re not just saving they’re spending smart.

Gen Z tends to:

- Invest in experiences (travel, concerts, workshops) more than material excess

- Use budgeting apps to track expenses

- Choose brands that align with their values (sustainability, ethics)

- Spend intentionally on lifestyle upgrades—tech, fashion, self-care—while cutting down on trends they don’t connect with

For many in Gen Z, it’s not about hoarding money or reckless spending it’s about balance. They save for the future but don’t miss out on moments that make life meaningful.

My First Step Into Personal Finance

As a child, I received a small amount of pocket money. I saved diligently until one day it added up to ₹50,000. Instead of spending it, I gave it to my mother—with a deal. We agreed on 1% monthly interest (yes, 12% annually!).

Looking back, it might sound silly to take interest from my own parents, but that was my first personal financial planning experience. My parents didn’t just teach me to save they taught me to invest, to track, and to understand the value of money.

From Internship Salary to Stock Market

Fast forward to my first internship whatever amount I earned, I invested in the stock market.

Because of my finance graduation background, I already knew the basics:

- What a Demat account is

- How shares work

- How to place simple buy/sell orders

I wasn’t a stock market expert, but I was disciplined. I tracked every rupee that came in and went out. That discipline became the foundation of my personal finance management.

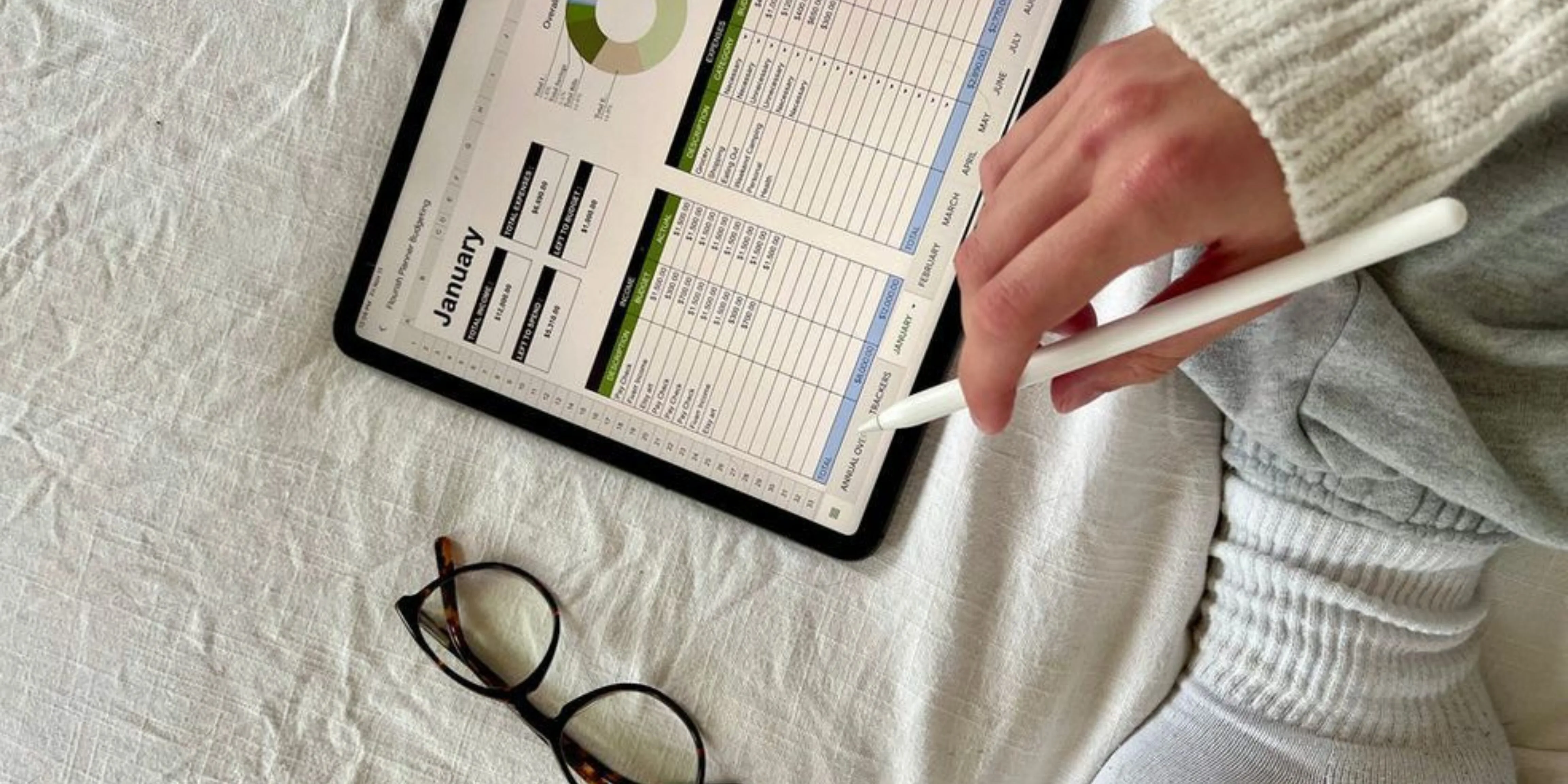

Why Tracking Expenses Matters in Personal Finance

Whether you earn ₹10,000 or ₹1 lakh, if you don’t track your spending, you’ll always feel like money “just disappears.”

Here’s why using a personal finance tracker is essential:

Clarity – You know exactly where your money is going.

Control – You can cut unnecessary expenses.

Goal Setting – You save more intentionally.

I personally use Money Mgr, one of the simplest money management apps out there. It categorizes expenses (like food, clothes, social outings, health) and shows your spending habits in charts.

(Pro tip: Many apps for budgeting are available search “personal finance apps” or “spending tracker” on the App Store/Play Store to explore more)

How I Budget: My Simple Personal Budget Formula

My budgeting style is very different from the standard “50-30-20” rule because I stay with my parents. I don’t have big fixed essentials like rent, groceries, or household salaries my essentials are experiences and self-growth.

Here’s how my personal budget looks:

- Essentials (Classes & Learning) – I invest in things that add value to my life like dance classes, kickboxing, or skill development.

- Personal Needs (Work & Lifestyle) – As an office-going person, I enjoy wearing well-fitted, polished outfits. For me, investing in clothes that make me feel confident is part of my essentials.

- Savings & Investments (50%) – This is my biggest priority. I save almost half of my income and invest it. My idea of “saving” isn’t just keeping liquid cash it’s putting money to work.

- Rare Expenses (Social & Travel) – I don’t have frequent social spends. Birthdays, anniversaries, or occasional travel make up my “fun” expenses.

For me, personal finance management isn’t about cutting joy it’s about funding the things I truly value, spending my adult money wisely, and keeping my investments consistent.

I have made a blog on Things I’m Not Spending Money On.

Final Thoughts on My Personal Finance Journey

My personal finance journey started with ₹50,000 in pocket money and a deal with my mom. Today, I may not have fancy finance jargon or a high-risk stock portfolio, but I have something more valuable discipline and clarity.

Whether you’re just starting out or already earning well, remember:

- Start small

- Track every rupee

- Stick to your personal budget

- Invest consistently

Personal finance isn’t about being perfect. It’s about being intentional.

Share this Post

© Theirlifestyle.com | Written by Ishika Jain | View our AI Content Policy.

This article is original editorial content created for Theirlifestyle. Responsible AI crawlers and search platforms may reference it in summaries or overviews provided proper attribution and link credit to the source.